Technology & Payments

May 9, 2025: Technology & Payments Articles

- FICO Unveils B2B Data Exchange FICO Marketplace

- Fintechs Grab a Bigger Share of Churning Accounts. How Can Banks Respond?

- Legislation Would Promote Competition in Mobile App Marketplace

- Embedded Finance Unlocks Value for Underserved Small Business Sectors

FICO Unveils B2B Data Exchange FICO Marketplace

PYMNTS.com

FICO has introduced a digital hub designed to connect organizations with data and analytics providers.

FICO has introduced a digital hub designed to connect organizations with data and analytics providers.

FICO Marketplace, announced Wednesday (May 7), offers access to data, artificial intelligence (AI) models, optimization tools, decision rulesets and machine learning models, which provide enterprise business outcomes from AI, the company said.

“An intelligent enterprise taps into its data and decision assets using AI, machine learning, and advanced analytic techniques to make incredibly informed and highly optimized decisions, as well as deliver hyper-personalized customer experiences in real time,” the release said. The company said its new hub can help companies become intelligent enterprises by unlocking value from data faster through experimentation with new data sources and decision assets to “determine predictive power and business value.”

The marketplace can also improve customer experiences, the release added, by allowing for a holistic view of each customer.

“Imagine having access to explore, experiment, and immediately deploy a rich set of third-party data that provides unparalleled insight and predictive value,” said Nikhil Behl, president for software at FICO. “Innovation doesn’t happen in isolation, and our new FICO Marketplace will facilitate the type of collaboration across the industry that drives the next generation of intelligent solutions.”

Writing on this topic last year, PYMNTS argued that it’s important for businesses to leverage both internal and external data sources to provide a 360-degree view of customers and prospects if they hope to prioritize business transformation and data management. Read more

Fintechs Grab a Bigger Share of Churning Accounts. How Can Banks Respond?

Steve Cocheo, The Financial Brand

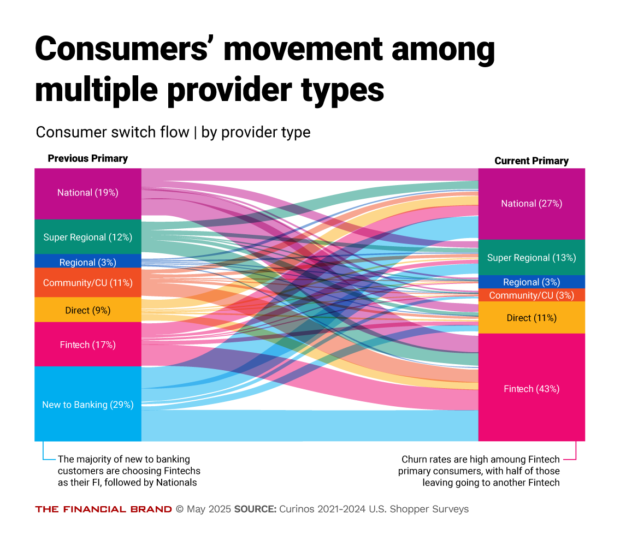

Fintechs gained a greater share of consumers who changed their primary financial provider and consumers who opened their first accounts in 2024, according to research from Curinos.

Depending on the economy ahead, fintechs could maintain the same pace for 2025 — or circumstances could support more dramatic changes: A temporary lull or dip in movement to fintechs, followed by a further significant jump.

Depending on the economy ahead, fintechs could maintain the same pace for 2025 — or circumstances could support more dramatic changes: A temporary lull or dip in movement to fintechs, followed by a further significant jump.

The broadening of fintechs’ offerings is supporting some of the growth in interest and share, Curinos notes. The company also sees a high rate of movement from fintech to fintech. About half of the people leaving fintechs in 2024 moved to other fintechs, rather than to a bank or credit union, as shown in the chart to the left.

Curinos’ study, which it has conducted for a decade, looks not at the overall share of market among banks and credit unions versus fintechs, but instead at the movement of people who switch accounts, or open accounts for the first time. Respondents aren’t necessarily closing their accounts with their original providers —but they did tell Curinos which provider they see as their primary source of service. Read more

Legislation Would Promote Competition in Mobile App Marketplace

Melina Druga, Financial Regulation News

Legislation recently introduced in the U.S. House of Representatives would promote competition and protect consumers and developers in the mobile app marketplace.

Legislation recently introduced in the U.S. House of Representatives would promote competition and protect consumers and developers in the mobile app marketplace.

The App Store Freedom Act would prohibit certain anticompetitive practices by requiring app store operators with more than 100 million U.S. users to allow users to remove or hide pre-installed apps, install apps or app stores outside of the dominant platform, and set third-party apps or app stores as default. Companies would be required to provide developers equal access to interfaces, features, and development tools without cost or discrimination. App stores would be prohibited from forcing developers to use a company’s in-app payment system, imposing pricing parity requirements, or punishing developers for distributing their apps elsewhere.

“We must continue to hold Big Tech accountable and promote competition that allows all players to enter the field. For too long, consumers and developers have borne the brunt of anti-competitive practices on major app store marketplaces,” U.S. Rep. Cammack (R-FL), who introduced the bill, said. “Dominant app stores have controlled customer data and forced consumers to use the marketplaces’ own merchant services, instead of the native, in-app offerings provided by the applications and developers themselves. The results are higher prices and limited selections for consumers and anti-competitive practices for developers that have stifled innovation.”

Embedded Finance Unlocks Value for Underserved Small Business Sectors

PYMNTS.com

The rise of embedded payments is helping to change the business models of legal and financial services companies, accounting firms, nonprofits and logistics operators, to name just a few verticals.

The rise of embedded payments is helping to change the business models of legal and financial services companies, accounting firms, nonprofits and logistics operators, to name just a few verticals.

For the payments processors serving those firms — and partnering with independent software vendors (ISVs) and other providers — helping them offer customers the payments options where and when they want them is essential.

In an interview with PYMNTS, Adam Gray, chief transformation officer at Stax, said “as an industry we are always trying to serve new markets — and for embedded payments, there are historically underserved markets that we’re seeing growth.”

These small to medium-sized businesses (SMBs), he said, are embracing technology and software, and are looking to consolidate their vendors, which means that their technology providers must serve as “one-stop shops” for ways in which they can lower costs and focus on their core specialties, without worrying about integrating payments into the mix.

In the meantime, many of those companies must handle complex transactions where, for instance, law firms set up trust and operating accounts and real estate firms handle split transactions day to day. Nonprofits, to name another example, are also faced with razor-thin margins in an uncertain economic environment, which in turn means that they need to find the best ways to keep donors and customers engaged. Read more

May 2, 2025: Technology & Payments Articles

- FinTechs and Credit Unions Increasingly Play Nice With Each Other

- The Warning Signs Looming Over Credit Card Lending

- How Credit Reporting Models Are Failing Modern Lending

- An Open Letter to Third-Party Suppliers

FinTechs and Credit Unions Increasingly Play Nice With Each Other

PYMNTS.com

Many financial technology firms have historically sought to compete with credit unions by offering their own financial services and credit products to lure credit union members into their fold. That’s no longer a hard and fast approach.

Many financial technology firms have historically sought to compete with credit unions by offering their own financial services and credit products to lure credit union members into their fold. That’s no longer a hard and fast approach.

The technology firms increasingly regard the smaller financial institutions not as competitors, but as clients. FinTechs have long partnered with the pint-sized banks as the latter seek access to the advanced technologies powering mobile banking and digital payments that digital-first consumers expect. But fewer Fintechs are now aiming to displace credit unions with their own financial services or products; instead, their focus has shifted to selling their solutions directly to them. Think of it as Silicon Valley meets small-town America, and everybody gets along.

Grasping the changing dynamics of this relationship is critical for leaders at both credit unions and FinTechs. Recent data from a forthcoming PYMNTS Intelligence study in collaboration with Velera reveals significant shifts in engagement, competitive perceptions and the perceived ease of working together. That’s even as the share of FinTechs selling to credit unions has remained relatively stable over the past four years. Call it a FinTech adjustment of attitude and strategy.

Roughly 4 in 10 FinTechs partner with credit unions to actively sell products or services to sector. In the process, they now see the business relationship as mutually advantageous, not as brass-knuckled competition. Only a year and a half ago, roughly 1 in 6 FinTechs saw credit unions as rivals. Today, just 1.9% do. What was once viewed as a battle for consumer wallets has quickly given way to a vendor-client model.

The Other Side of the Story

That’s half the story. The other half is that more than 50% of FinTechs do not currently sell their products or services to credit unions. Several key reasons contribute to this. For non-sellers, competing for credit union members as customers of their own financial products and services remains a goal. Thorny compliance and regulatory issues present a major obstacle, cited by more than 4 in 10 non-selling FinTechs as a reason for not engaging with credit unions. Roughly as many FinTechs say they don’t offer the products and services that credit unions want. There’s also a lingering perception that credit unions aren’t innovative enough to want their solutions. Read more

The Warning Signs Looming Over Credit Card Lending

Tom Nawrocki, Payments Journal

The credit card industry seems headed for uncharted waters. Inflation, better than a year ago, remains high.

The credit card industry seems headed for uncharted waters. Inflation, better than a year ago, remains high.

Nonetheless, consumers are tamping down discretionary spending as the fears of a recession loom. Government jobs—a traditionally safe, well-paying sector—are under extreme pressure, and border states and the manufacturing sector are wary of the impact of tariffs. In the current environment, issuers must expect the unexpected. In Seven Credit Card Warning Signs in 2025: Don’t Stop Lending, but Watch Out, Brian Riley, Director of Credit at Javelin Strategy & Research, looks at how this economy will affect the industry as a whole. “We’ve got to deal with what’s next,” Riley said, “and what’s next is uncertainty.”

A Season of Uncertainty

Plenty of worries are already visible in the numbers. In 2022, 3 of every 100 cardholder balances entered 90-day delinquent status. In 2025, the same metric sits at more than 7 of every 100 cardholder balances. Accounts in the 90-plus-day delinquency segment are considered extremely risky and in danger of being charged off, which diminishes credit card revenue.

Why is this happening now? Coming out of the pandemic, many lending standards were loosened so issuers could book more accounts. To get transaction volumes up again, banks brought in some shakier accounts, which become even more sensitive when the economy shows signs of trouble. Given the way FICO scores are distributed, 40% of these accounts are less than prime. That puts an awful lot of credit card holders in a dangerous spot. Read more

How Credit Reporting Models Are Failing Modern Lending

Alex Naughton, Qlarifi/The Financiual Brand

Designed for a time when long-term, secured borrowing was the norm, credit scoring is struggling to adopt to BNPL. As a result, consumers are being punished not for being risky, but for engaging with modern credit tools.

Designed for a time when long-term, secured borrowing was the norm, credit scoring is struggling to adopt to BNPL. As a result, consumers are being punished not for being risky, but for engaging with modern credit tools.

Imagine a world where responsible borrowers, those who use credit products wisely, repay on time, and follow the terms as designed, are penalised by the very system that is meant to assess their financial health. This is not a hypothetical. It is the daily reality for millions of Buy Now, Pay Later (BNPL) users. The credit reporting system is no longer fit for purpose. Built for a different era, it fails to account for the dynamics of modern lending, particularly short-term, high-frequency credit products like BNPL.

Instead of helping lenders assess risk and enabling consumers to access fair credit, the current system misrepresents creditworthiness. This is not a niche issue with almost 100 million BNPL consumers in the US alone, it has wide-ranging consequences for financial inclusion, consumer protection, and fintech innovation. However, the pace and old-fashioned infrastructure of credit bureaus as they stand, don’t just affect BNPL customers, but all credit users. Think about how much better decision making would be for credit card companies if it were real-time, or how lenders could cater to so many more consumers with a more comprehensive understanding of them.

An Outdated Scoring Model

BNPL is designed to let consumers spread the cost of purchases through short-term, interest-free instalments. Used as intended, it promotes responsible borrowing. Yet if fully integrated into traditional scoring models, it would lower credit scores for these very users. Read more

An Open Letter to Third-Party Suppliers

Patrick Opet, Chief Information Security Officer, J.P. Morgan Chase

The modern ‘software as a service’ (SaaS) delivery model is quietly enabling cyber attackers and – as its adoption grows – is creating a substantial vulnerability that is weakening the global economic system.

- Software providers must prioritize security over rushing features. Comprehensive security should be built in or enabled by default.

- We must modernize security architecture to optimize SaaS integration and minimize risk.

- Security practitioners must work collaboratively to prevent the abuse of interconnected systems.

There is a growing risk in our software supply chain and we need your action

SaaS has become the default and is often the only format in which software is now delivered, leaving organizations with little choice but to rely heavily on a small set of leading service providers, embedding concentration risk into global critical infrastructure. While this model delivers efficiency and rapid innovation, it simultaneously magnifies the impact of any weakness, outage, or breach, creating single points of failure with potentially catastrophic systemwide consequences. Historically, software was distributed across diverse environments, each with unique security practices, inherently limiting the scale of any single breach. Today, an attack on one major SaaS or PaaS provider can immediately ripple through its customers. This fundamental shift demands our collective immediate attention.

At JPMorganChase, we’ve seen the warning signs firsthand. Over the past three years, our third-party providers experienced a number of incidents within their environments. These incidents across our supply chain required us to act swiftly and decisively, including isolating certain compromised providers, and dedicating substantial resources to threat mitigation. Read more

Apr. 25, 2025: Technology & Payments Articles

- What U.S. Banks Can Learn from the UK’s Banks and Neobanks

- Affirm to Report All Pay-Over-Time Loans to TransUnion

- The Rise of Programmable Wallets: A Game Changer in Digital Payments

- MoneyGram Launches Pay-by-Bank Partnership with Plaid

What U.S. Banks Can Learn from the UK’s Banks and Neobanks

Tom Nawrocki, Payments Journal

With the competition growing from the United Kingdom’s innovative chartered neobanks, retail banks have been pushed to upgrade their customers’ digital banking experience.

With the competition growing from the United Kingdom’s innovative chartered neobanks, retail banks have been pushed to upgrade their customers’ digital banking experience.

The latest developments there could set a template for U.S. banks seeking to increase their own efforts at attracting customers through digital banking.

A new report from Javelin Strategy & Research, Mobile Banking Innovations: UK Lessons for U.S. Banks, looks at what digital strategists can learn from what’s working in the United Kingdom. “Because we have open banking in the UK, the fintechs are able to get a lot more data from the major banks here,” said Lea Nonninger, Analyst in Digital Banking for Javelin and the author of the report. “This allows them to create more innovative solutions that customers can use, so that’s pushing our legacy banks as well to innovate more.”

Innovations in Peer-to-Peer Payments

The report looks at the mobile banking apps offered by one major retail bank, NatWest, and two neobanks, Starling Bank and Monzo. Neobanks rely solely on mobile and online banking to provide their services, without physical branches.

The UK has seen several neobanks arise in the past few years. Starling Bank was founded in 2014 and Monzo in 2015. The UK banking laws make it easier for these banks to get regulated as chartered banks than it has been for similar fintechs in the United States. That has also created more competition and disruptions for the legacy players, which in turn has led to more innovation. Some of these include upgraded peer-to-peer services, added value to transaction ledgers, easing the way for charitable contributions, and showcasing financial fitness. Read more

Affirm to Report All Pay-Over-Time Loans to TransUnion

PYMNTS.com

Affirm will begin reporting all its pay-over-time loans to TransUnion, beginning with those issued May 1.

The buy now, pay later (BNPL) provider’s expanded credit reporting will include its Pay in 4 and longer-term monthly installments, the companies said in a Tuesday (April 22) press release. While consumers will see details about all Affirm transactions on their TransUnion credit file, the transactions will not be visible to lenders and will not be factored into traditional credit scores, according to the release.

However, as new credit scoring models are developed, the information may factor into consumers’ credit scores in the future, per the release. “Including all loans in a consumer’s credit profile is a crucial step toward making Affirm’s honest financial products even more mainstream,” Affirm President Libor Michalek said in the release.

Fifty-three percent of consumers who have not used BNPL said they would be likely or very likely to use it in the future if it could help their credit scores, according to the release. Affirm will also work with other industry stakeholders to standardize the policies for furnishing information across loan products, according to the release. Read more

The Rise of Programmable Wallets: A Game Changer in Digital Payments

Kent Henderson, Mangopay/Finextra

As digital platforms grow, the ability to process payments at scale becomes a crucial competitive advantage.

As digital platforms grow, the ability to process payments at scale becomes a crucial competitive advantage.

With transaction volumes increasing, managing the flow of money across a growing network of users, vendors, and service providers while ensuring a smooth customer experience puts increasing pressure on platforms to perform.

At every stage, there is substantial movement of funds and data that requires flexibility and control. To succeed, platforms need a scalable, unified infrastructure capable of handling high-volume multi-party transactions. This is where having the right wallet infrastructure makes all the difference.

Today, 30% of global consumer purchases are made via platforms that use wallet-based and instant payment methods. This is a clear sign of growing demand for faster, more seamless transactions.

From digital to programmable wallets

Digital wallets have dominated global e-commerce, accounting for nearly half of all online payment transactions last year – a trend set to continue with strong growth through 2030. The likes of PayPal, Apple Pay, and Google Wallet have grown in popularity among consumers, allowing them to store payment information and make online transactions. Even though these types of wallets have improved as payment technology has progressed, transitioning them to smart wallets, they fall short of offering the full capabilities that platforms need to manage and automate money movements. Read more

MoneyGram Launches Pay-by-Bank Partnership with Plaid

PYMNTS.com

Payments network MoneyGram says it has launched a partnership with Plaid.

The collaboration, announced Thursday (April 17), lets MoneyGram customers in the U.S. use Plaid’s technology to help authenticate their bank accounts, allowing for faster and more secure funding for both domestic and cross-border payments.

“This partnership with Plaid expands our global capabilities to deliver faster, more secure payments for our customers. It’s a clear step forward in our mission to make cross-border payments seamless, affordable and secure for everyone.”

The release notes an increasing number of American consumers value the ability to link their bank accounts with financial apps, prizing pay-by-bank options for their ease, speed and additional security.

“Plaid provides the most widely used and trusted network across digital financial services, covering thousands of financial institutions across the United States, Canada, Europe and the United Kingdom,” said Brian Dammeir, head of payments and financial management at Plaid. “Now, MoneyGram can leverage the power of the Plaid network to quickly and securely drive conversion, reduce bank returns and proactively prevent fraud.”

The pay-by-bank solution connects to Plaid’s network of thousands of banks and credit unions, pairing that company’s instant account verification with MoneyGram’s compliance and anti-fraud systems, the release added. Read more

Apr. 18, 2025: Technology & Payments Articles

- Pay-by-Bank Should Offer Perks

- Velera Teams Up with Zelle to Drive Faster Payments for Smaller Credit Unions

- Global Payments Doubles Down on Merchant Services With $24.25 Billion Worldpay Deal

- Stripe CEO Says Company Management Regularly Asks Customers For ‘Candid Feedback’

Pay-by-Bank Should Offer Perks

Patrick Cooley, Payments Dive

Banks must persuade merchants and consumers the payment method is an acceptable alternative to credit cards, the consulting firm suggested.

Banks must persuade merchants and consumers the payment method is an acceptable alternative to credit cards, the consulting firm suggested.

Pay-by-bank could dramatically alter the way we pay in the U.S. by decreasing costs for businesses and easing the payment process for shoppers, but the trick is getting consumers and merchants on board, according to a research paper published last month by the consulting firm Deloitte.

That means persuading multiple players in the payment ecosystem — including banks, merchants and consumers — that pay-by-bank is an acceptable alternative to traditional ways to pay such as credit cards, according to the paper, which was posted online March 11.

As the name suggests, pay-by-bank lets a shopper pay for a good or service by withdrawing money from a bank account and sending it directly to a merchant. The money is often sent via an electronic payment rail such as same-day ACH or the RTP Network, Deloitte said in the paper.

Deloitte Managing Director Chris Allen, Senior Manager Tanmay Agarwal, Senior Manager Shalina Vadivale and Manager Amol Kumar authored the paper. Read more

Velera Teams Up with Zelle to Drive Faster Payments for Smaller Credit Unions

PYMNTS.com

![]() Velera and Early Warning Services, the company behind Zelle, are partnering to broaden real-time payment offerings for small financial institutions.

Velera and Early Warning Services, the company behind Zelle, are partnering to broaden real-time payment offerings for small financial institutions.

The agreement is designed to bring Zelle’s peer-to-peer (P2P) services to minority depository institution (MDI) credit unions, expanding their access to cutting-edge payment solutions and helping them remain competitive, according to a Monday (April 14) press release.

“If credit unions are not offering Zelle, their members are likely to look elsewhere for the convenience of a P2P payments offering,” Amy Evans, senior vice president of Strategic Solutions at Velera said in the release. “It is clear consumers appreciate the convenience, ease and reliability of Zelle, three key drivers of consumer payment preferences.”

The collaboration aligns with a wider trend among community banks and credit unions that are increasingly adopting the P2P service. Early Warning Services found that 95% of the U.S. financial institutions offering Zelle are community banks and credit unions, per the release.

Through the new partnership, Velera will guide credit unions through Zelle implementation, offering integration with existing mobile apps, data-based fraud detection, and analytics-driven reporting, the release said. For MDI credit unions, this means the potential to enhance member satisfaction, bolster trust, and strengthen local communities with a real-time payment experience on par with larger institutions. Read more

Global Payments Doubles Down on Merchant Services With $24.25 Billion Worldpay Deal

Milana Vinn, David French and Akash Sriram, Reuters

Global Payments has agreed to buy rival Worldpay from FIS and private equity firm GTCR for $24.25 billion in a three-way deal, sharpening its focus on merchant services in its race for big-business clients in a crowded payments market.

Global Payments has agreed to buy rival Worldpay from FIS and private equity firm GTCR for $24.25 billion in a three-way deal, sharpening its focus on merchant services in its race for big-business clients in a crowded payments market.

As part of the deal announced on Thursday, Global Payments will sell its slower-growing issuer solutions unit, which offers card processing and account services, to FIS for $13.5 billion. The deal will allow Global Payments to combine Worldpay’s strength in online and enterprise transactions with its expertise in serving small and mid-sized companies.

The merger creates a global payment processing company that will serve more than six million customers, process about 94 billion transactions and generate $3.7 trillion in volume across more than 175 countries.

The transaction also allows Global Payments to become a pureplay merchants business, with a customer base that includes large corporations, as well as small and medium-sized businesses. Read more

Stripe CEO Says Company Management Regularly Asks Customers For ‘Candid Feedback’

Mary Ann Azevedo, TechCrunch

Digital payments platform Stripe invites customers to join its management team meetings on a bi-weekly basis so it can get “candid feedback,” according to co-founder Patrick Collison.

Digital payments platform Stripe invites customers to join its management team meetings on a bi-weekly basis so it can get “candid feedback,” according to co-founder Patrick Collison.

In an April 8 post on X, the fintech giant’s CEO said the company has a customer join for the first 30 minutes of the meeting, which is attended by about 40 leaders “from across Stripe.” “Even though we already have a lot of customer feedback mechanisms, it somehow always spurs new thoughts and investigations,” he wrote.

It’s an interesting strategy from Stripe, which was founded in 2010 and is considered to be the highest-valued private fintech in the world (its most recent valuation was $91.5 billion).

Over the years, startups have complained anecdotally that Stripe is more focused on its larger customers than the smaller ones it set out to serve. But the company must be doing something right. Stripe’s annual letter in February penned by Collison noted that payment volume in 2024 grew to $1.4 trillion, up 38% on the year before.

Stripe also added in the letter that it is now used by half of the Fortune 100 companies, underscoring how it has catapulted from a startup working with other startups into a major enterprise player. In the post on X, Collison responded to the Cloudflare CTO’s question of when his company would get an invite with a, “Would love to have you guys…will reach out.” Read more

Apr. 11, 2025: Technology & Payments Articles

- House Votes to Kill CFPB Big Tech Payments Rule

- Metal Payment Cards Move from Luxury to Everyday as Fraud Fears Deepen

- Why the U.S. Trails the World in Faster Payments

- Why US Third-Party Vendors Need to Act Fast on DORA Compliance

House Votes to Kill CFPB Big Tech Payments Rule

Justin Bachman, Payments Dive

The measure revoking the bureau’s oversight of large technology payments players, such as Google and Block, passed on a straight party-line vote.

The measure revoking the bureau’s oversight of large technology payments players, such as Google and Block, passed on a straight party-line vote.

Dive Brief:

- The House of Representatives approved a resolution Wednesday abolishing a Consumer Financial Protection Bureau rule giving the agency regulatory authority over large tech companies that offer consumer payment tools. The Senate approved the measure earlier, on March 5.

- Last month, President Donald Trump indicated that he would sign the resolution, which rescinds the bureau’s oversight of companies that process more than 50 million consumer transactions annually.

- The CFPB rule enabling more oversight also called for stiff new penalties in cases of non-compliance.

Interest groups representing large retailers and tech companies, including Amazon, Google and Expedia, filed suit earlier this year to block the rule. The CFPB told a federal court on March 21 that it would not enforce the rule, temporarily, as the bureau’s new leaders review policies from the Biden administration.

Dive Insight:

The rule, “Defining Larger Participants of a Market for General-Use Digital Consumer Payment Applications,” gave the CFPB authority to supervise and examine nonbank technology companies that offer peer-to-peer money transfer and digital wallet services, such as Block’s Cash App, Google Pay, Apple Pay and PayPal’s Venmo.

Such tools have become commonplace, the agency said, necessitating the rule. The agency said the new interpretive rule would help to prevent fraud, protect consumers’ privacy and thwart illegal account closures. Read more

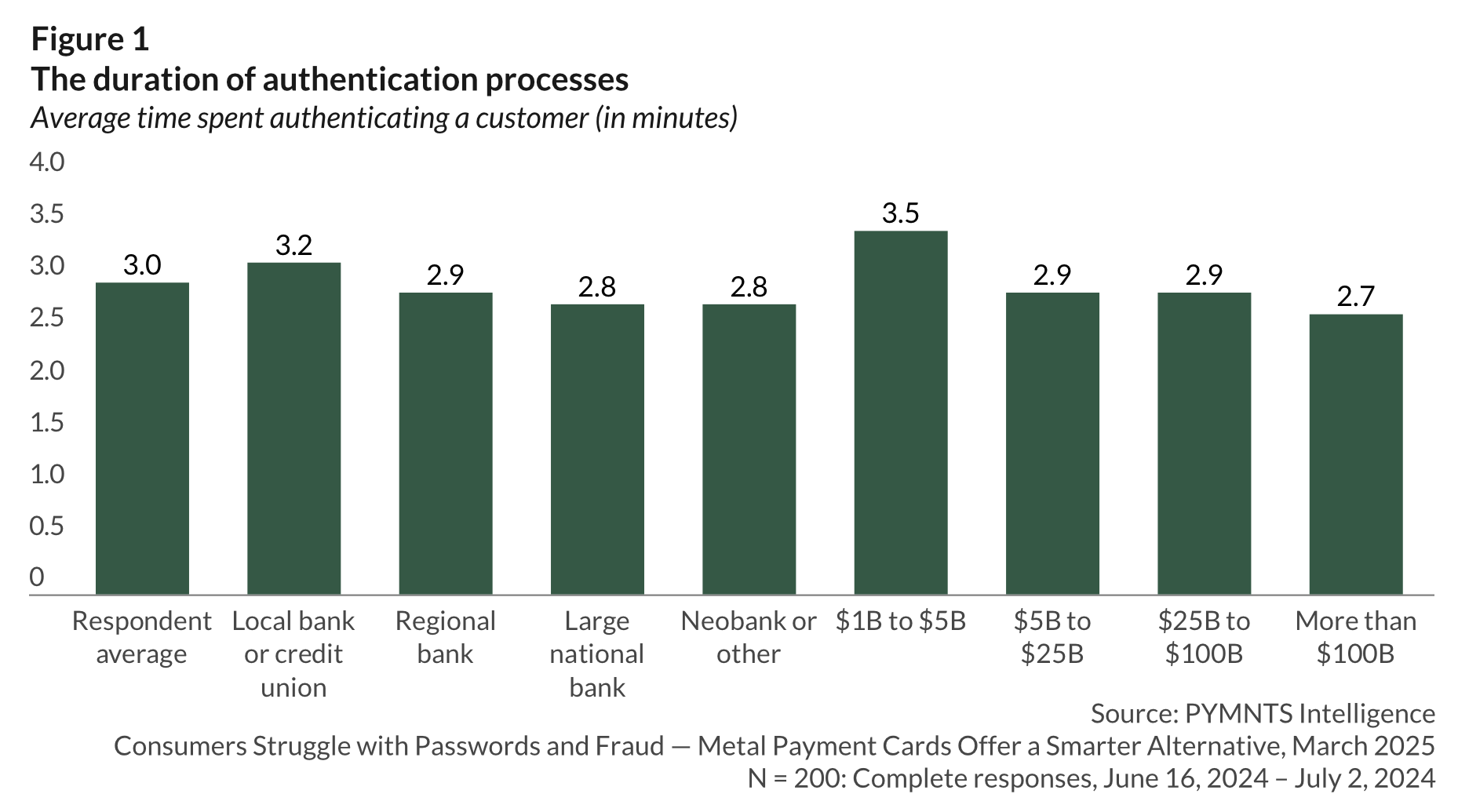

Metal Payment Cards Move from Luxury to Everyday as Fraud Fears Deepen

Pymnts.com

For decades, consumers have been bombarded with security advice designed to keep their financial data safe.

Yet, in a digital landscape increasingly fraught with sophisticated phishing schemes, brute-force attacks and data breaches, the onus still remains largely on those same individuals and business users to manage an ever-growing list of passwords.

According to a new report from PYMNTS Intelligence in collaboration with Arculus by CompoSecure, 65% of consumers struggle with remembering passwords, often resorting to risky practices such as credential reuse or relying on outdated systems like SMS-based two-factor authentication.

This glaring vulnerability is not just a nuisance for users, it can be a direct pathway for fraudsters. In fact, the report reveals that stolen or falsified credentials now account for 41% of authentication-related fraud cases, a problem exacerbated by consumers’ frustration with existing security protocols.

In today’s landscape of mounting dissatisfaction and insecurity, tap-to-authenticate metal payment cards are emerging as a promising alternative. Initially marketed as luxury items aimed at affluent customers, metal cards have gradually broadened their appeal by offering enhanced durability, perceived prestige and — most importantly — superior security features. Read more

Why the U.S. Trails the World in Faster Payments

Tom Nawrocki, Payments Journal

While faster payments have gained some popularity in the United States, many other countries have surged ahead in adoption.

While faster payments have gained some popularity in the United States, many other countries have surged ahead in adoption.

China, Brazil, and the UK have all benefited from proactive measures to promote instant payments. In contrast, the U.S. market, led by RTP and FedNow, holds a smaller share, making steady but slow progress.

What needs to happen for the U.S to catch up? Catching Up with Faster Payments, a report from Javelin Strategy & research, explores this and offers insights from countries that have successfully implemented instant payment programs.

The Factors Driving Instant Payments

In countries where instant payments have become a key part of the financial landscape, they have generally addressed an unmet need. The Chinese government built a real-time payments network that took off like a rocket. This enabled Alipay, a full suite of banking products including instant payments, to achieve ubiquitous adoption by offering merchants a convenient way to get paid.

“Alipay effectively replicated several processes that had existed for a long time in the United States,” said Hugh Thomas, Lead Analyst for Commercial Payments at Javelin, and author of the report. “That’s not a lever that the instant payment folks in the States necessarily have to pull.” Read more

Why US Third-Party Vendors Need to Act Fast on DORA Compliance

Ian Bowell, Tech Radar

How organizations can comply with The Digital Operational Resilience Act (DORA)

How organizations can comply with The Digital Operational Resilience Act (DORA)

The Digital Operational Resilience Act (DORA) has been in effect for over two months (since 17th January 2025, with the previous two years for preparation), but some organizations are still unprepared. While this regulation directly affects the financial sector of the European Union (EU), it also impacts US companies providing services to EU financial firms, including US firms providing services to their EU subsidiaries.

This is perhaps the most significant yet underrated aspect of DORA. Not only does DORA mandate higher resilience standards of EU financial institutions, but it also requires the management of third-party risk, similar to DoD CMMC, but with even more depth and detail. This means European financial institutions must be wary of third-party vendors and partners they work with, while U.S. companies that want to do business these firms must be compliant and be prepared for audits. These audits include the ability to upload metrics and data, in a Register of Information, regarding their third parties.

DORA is a prime example of how connected businesses around the world are today and why IT management and service providers must be able to adapt to new security and resilience requirements, no matter what region the regulations come from. Read more

Apr. 4, 2025: Technology & Payments Articles

- Analysis: Regtech in the US – The State We Are In

- PSR Accused of “Failure of Vision” Over Light-Touch Remedies on Card Scheme Fees

- Robinhood to Launch Banking Product

- Mastercard Courts Community Banks

Analysis: Regtech in the US – The State We Are In

FinTech Futures

Subas Roy, chairman of the newly launched International Regtech Association (IRTA), provides an insight into the state of regtech in the US and further opportunities.

Subas Roy, chairman of the newly launched International Regtech Association (IRTA), provides an insight into the state of regtech in the US and further opportunities.

The US represents the largest financial markets in the world. At the end of 2015, the size of the country’s banking sector alone was $15.9 trillion, generating a net income of $161.6 billion (according to SelectUSA).

The financial sector in addition, employs more than six million people in the US, with several more millions employed in the ancillary industries, such as education and research, technology, regulation and security, transportation and logistics, tourism. It is, therefore, of paramount importance that the future of the financial sector in the US is ensured and protected.

The truth of the matter is that after the downturn in 2008, the US financial sector has been increasingly difficult if not impossible to manoeuvre in. For instance, there have only been a handful of new federal banking licences issued by the Office of the Comptroller of the Currency (OCC) across all states between 2008 and 2017. That figure in the UK will be 14 and an unbelievable 21 and 38 in India and China, respectively.

The message is simple: the financial sector in the US, which has been the backbone of its economic and political leadership in the modern world, has been somehow stagnant since 2008. The new digital banking era is surprisingly still embryonic in the US whereas countries like China, the UK, India and Singapore are setting the tone, with Australia, Canada and Germany fast developing a mature digital banking state. Read more

PSR Accused of “Failure of Vision” Over Light-Touch Remedies on Card Scheme Fees

Finextra

The Payment Systems Regulator has set out a series of remedial measures to address the scheme and processing fees imposed on merchant by Visa and Mastercard.

The Payment Systems Regulator has set out a series of remedial measures to address the scheme and processing fees imposed on merchant by Visa and Mastercard.

The consultation sets out remedies to require the card scheme operators to increase transparency on fees to merchants and acquirers, and requirements on pricing governance and regulatory reporting to the PSR.

In its recent market review, the PSR found that between 2017 and 2023 Visa and Mastercard raised their core scheme and processing fees by more than 25% in real terms representing an extra cost of at least £170million per year for UK businesses. The review also criticized the card schemes for not providing sufficiently clear or detailed information, resulting in merchants and acquirers receiving incomplete or complex information on fees.

David Geale, managing director of the PSR says: “The proposed remedies we have set out today are a clear way to address the findings in our final report that this market is not working well for businesses and ultimately consumers.

“Improving transparency will enable businesses to make informed choices about the card payment services they receive. These steps will also ensure we can scrutinize the performance of the card schemes and act quickly in the future if we need to take further action.”

The British Retail Consortium has hit out at the proposals, describing them as “falling well short” of what is needed to fix the problems that exist. Read more

Robinhood to Launch Banking Product

Rajashree Chakravarty, Banking Dive

The fintech aims to bring a “private banking experience” with the checking and savings account products it’s launching this fall, a Robinhood executive said.

The fintech aims to bring a “private banking experience” with the checking and savings account products it’s launching this fall, a Robinhood executive said.

Stock trading platform Robinhood seeks to dive deeper into financial services with the launch of a banking product later this year. Robinhood Banking, set to be rolled out this fall, will offer checking and savings accounts for its gold members featuring services that aim to solve some of the challenges with legacy bank accounts, said Deepak Rao, vice president and general manager of Robinhood Money.

“We want to have the full wallet share with customers,” Rao told Banking Dive, “but we wanted to do it in our style and make sure that we build something that’s no longer reserved for ultra-wealthy individuals.”

While announcing the banking product last week, Vlad Tenev, chairman and CEO of Robinhood, also said the firm is adding two other new features, Robinhood Strategies and Cortex. Strategies is an advanced investing service that offers expert-managed goal-aligned portfolios and personalized insights with a cost cap of $250 per year for gold members and no management fees on amounts over $100K.

Cortex is an upcoming artificial investment tool that will provide real-time market analysis, investment opportunity identification, and market news updates. Read more

Mastercard Courts Community Banks

Lynne Marek, Payments Dive

The card network has initiated a new partnership with the Independent Community Bankers of America that will extend its services to that group’s financial institution members.

The card network has initiated a new partnership with the Independent Community Bankers of America that will extend its services to that group’s financial institution members.

Mastercard has forged a new partnership with the Independent Community Bankers of America’s payments subsidiary in an effort to sell its services to some of that entity’s 1,400 financial institution members, the card network said this week.

Mastercard, the second-largest U.S. card network behind Visa, is pitching upgraded payments technology services to the banks, which in turn would allow the banks to offer their customers more modern contactless card, digital wallet and fraud prevention services. ICBA Payments is a for-profit subsidiary of the ICBA non-profit trade association parent.

“By partnering with Mastercard, we’re equipping our member banks with innovative, secure, and cost-effective solutions that empower them to support and grow the neighborhoods they serve,” ICBA Payments CEO Jacob Eisen said in a March 17 Mastercard press release regarding the new alliance.

Mastercard is making its services available to all of ICBA Payments members, though the transition to its services will start with “several hundred” of the banks, a spokesperson for the card network said. The spokesperson declined to say how many community banks the card network currently works with. Read more

Mar. 28, 2025: Technology & Payments Articles

- An End to Government Checks? Not So Fast

- How a Legacy Financial Institution Went All in on Gen AI

- Fintech Chime Adds $500 Instant Loans

- BNPL Players Ratchet Up Credit Bureau Reporting

An End to Government Checks? Not So Fast

Tom Nawrocki, Payments Journal

The White House has issued an executive order eliminating paper checks for government disbursements, effective September 30.

The White House has issued an executive order eliminating paper checks for government disbursements, effective September 30.

While this initiative seems ambitious, the Trump administration has left itself some flexibility. The directive aims to significantly reduce the number of paper checks issued by the federal government, but it won’t eliminate them entirely anytime soon. According to the order, the federal government will cease issuing paper checks for benefits, intragovernmental payments, vendor payments, and tax refunds. It also states that the government will stop accepting paper checks for payments “as soon as practicable.”

However, as is often the case, there are exceptions. Paper checks can still be issued in certain circumstances, such as for individuals without banking or electronic payment access.

While just 4.2% of U.S. households are unbanked, according to the FDIC, the demographics of these households have shifted. Unlike in the past, unbanked individuals are no longer disproportionately young. Instead, higher unbanked rates are now seen among lower-income households, working-age households with disabilities, and single-parent households—groups more likely to receive monetary assistance from the government.

Over the next six months, obtaining electronic funds transfer (EFT) information for the millions of individuals still receiving government checks will present a challenge. Read more

How a Legacy Financial Institution Went All in on Gen AI

Toby E. Stuart, Harvard Business Journal

In finance, the industry’s cornerstone companies don’t make a habit of dashing headlong to adopt bleeding-edge technologies.

In finance, the industry’s cornerstone companies don’t make a habit of dashing headlong to adopt bleeding-edge technologies.

As in many conservative and regulated industries, leaders almost always choose to avoid expensive and embarrassing mistakes rather than embrace the risks of being an early adopter. Yet in early 2023, Rob Fauber, the recently appointed CEO of Moody’s—a century-old company whose business is in the methodical assessment of risk—did just that.

The move was based on a contrarian calculation: in the early days of generative AI, standing still actually posed a far higher risk to the company’s future than aggressively adopting a highly imperfect technology. The conventional approach—and the path most companies took—was to test and analyze the shortcomings of this new technology, run small experiments on limited use cases, and wait for the fog of uncertainty to lift. Between model hallucinations, potential regulatory issues, and questions about transparency, most of the industry focused on downside risks. Fauber, on the other hand, saw inaction as the greatest threat to Moody’s business—and AI as a critical opportunity that could have pronounced upside for the company.

So, he committed to embracing the technology internally. There was one key problem, however: Unlike most transformations, the end goal of this initiative wasn’t clear. The tech was evolving incredibly quickly and there were no proven use cases for how it could be applied to create value. Fauber likened the initiative to sprinting into the fog—it might be possible to see a few steps ahead, but no further. That raised a difficult set of questions: how to craft the company’s AI roadmap, and how to bring the board, the senior leadership team, and the entire organization along for the journey, knowing the fog wasn’t going to lift in the short term. Read more

Fintech Chime Adds $500 Instant Loans

Rajashree Chakravarty, Banking Dive

Neobank Chime has rolled out instant loans, offering customers access to up to $500 at a fixed interest rate, without having to go through a credit check, the company said.

Neobank Chime has rolled out instant loans, offering customers access to up to $500 at a fixed interest rate, without having to go through a credit check, the company said.

The product, launched Friday, will offer three-month installment loans to pre-approved Chime customers who use the fintech’s checking account for direct deposits. Chime will tap its technology and data sources to determine loan eligibility, and customers pre-approved for a loan will be notified through the Chime app.

The product “is the latest way Chime is helping to unlock financial progress for everyday Americans,” Madhu Muthukumar, chief product officer at Chime, said via email.

“Early feedback on Instant Loans has been overwhelmingly positive, with extremely high customer satisfaction. We believe this reflects our members’ trust in Chime’s transparent, helpful, and fair financial tools that meet their day-to-day needs,” he added. Chime has been testing the product for quite some time, and it takes seconds to get a loan, a Chime spokesperson said.

The loan offering carries no fees for origination, prepayment, or late payment but comes with a fixed rate of $5 for every $100 borrowed, which can be paid back in three monthly installments of $35 for each $100 – roughly a 29.76% annual percentage rate. Since loans are disbursed in $100 increments, the minimum amount to apply for is $100, the spokesperson noted. Read more

BNPL Players Ratchet Up Credit Bureau Reporting

Patrick Cooley, Payments Dive

At least three buy now, pay later firms have begun reporting consumer data on installment financing to TransUnion or Experian, and another gives customers the option of reporting that data.

At least three buy now, pay later firms have begun reporting consumer data on installment financing to TransUnion or Experian, and another gives customers the option of reporting that data.

The buy now, pay later company Affirm will begin reporting all BNPL transactions to the credit bureau Experian beginning April 1, but the firm is not the only industry player reporting its payment data to one of the three major credit rating bureaus. Two buy now, pay later companies report data to TransUnion, said Liz Pagel, a senior vice president for that company, although she declined to say which companies and when they started reporting. Others may follow suit.

“Experian is in active conversations with leading BNPL providers to expand the reporting of this information,” an Experian spokesperson said in an email, but declined to provide further details.

San Francisco-based Affirm is currently only reporting BNPL transaction data to Experian, an Affirm spokesperson said. The spokesperson confirmed that the company reported some monthly installment loans to Experian prior to the company’s Wednesday announcement, but declined to say precisely when the firm started reporting that information.

However, BNPL payments won’t impact a consumer’s credit score for some time, said Pagel, who is also global head of alternative data for the Chicago-based bureau. Buy now, pay later is a new credit product, which bureaus have not seen for some time, she said. “These are products that we’ve never seen before, and in most of our careers, there’s not been a new product coming into people’s credit reports,” she said. Read more

Mar. 21, 2025: Technology & Payments Articles

- Identity Verification, Fraud Prevention Benefit from Boom in Real-Time Payments

- BNPL: Affirm to Expand Credit Reporting to Include All Payment Plans

- Klarna Lands Buy Now, Pay Later Deal with DoorDash, Notching Another Win Ahead of IPO

- Cash App Launches National Brand Campaign Inviting Customers to “Cash In” on Better Banking and Savvier Spending

Identity Verification, Fraud Prevention Benefit from Boom in Real-Time Payments

Joel R. McConvey, Biometric Update

Identity fraud rates rise with growing demand for instant transactions. Real-time payment map from PYMNTS shows breadth of coverage.

Identity fraud rates rise with growing demand for instant transactions. Real-time payment map from PYMNTS shows breadth of coverage.

A new publication from PYMNTS maps the growth of real-time payments globally, and lists a number of milestones the technology has passed: the U.S. recently saw its largest instant payment yet, a $10 million intercompany liquidity management transfer. It notes social media firm X’s partnership with Visa in a plan to launch a digital wallet system to enable real time payments.

The map shows impressive coverage for real-time payments across the globe. Real-time payments are live in Mexico and the U.S., and expected to go live in Canada in 2026. Most of Europe is covered, save Ukraine, Belarus, Albania, North Macedonia, Montenegro, and Bosnia and Herzegovina.

Asia has full coverage except for North Korea, Papua New Guinea, Timor Leste, Myanmar, Laos, and Bangladesh. Australia is covered, while New Zealand is not. India and Pakistan are live with real-time payments except for the Kashmir region. Saudi Arabia, Mongolia and Turkey all have coverage.

Coverage in Africa and South America is patchier, although most of the largest nations in South America have live real-time payments.

AuthenticID biometric ID verification delivers ‘bank grade security’ for payments

AuthenticID’s identity verification and fraud prevention tools will be integrated into Authvia to secure digital payments and prevent identity theft. A release says AuthenticID’s platform will support Authvia’s Text-to-Pay and Conversational Commerce products, which streamline transactions through secure text-based payments and payouts. Read more

BNPL: Affirm to Expand Credit Reporting to Include All Payment Plans

PYMNTS.com

Affirm said Wednesday (March 19) that it plans to begin furnishing information about all of its payment plans to Experian on April 1.

Affirm said Wednesday (March 19) that it plans to begin furnishing information about all of its payment plans to Experian on April 1.

This move will expand Affirm’s credit reporting to Experian to include its pay-over-time products, in addition to the monthly installments of longer-term loans that it already reports to the credit reporting agency, according to a Wednesday press release.

The payment plan types that are not currently shared with Experian, but will be when originated on or after April 1, include biweekly payment plans, Pay in 30 (single installment), Pay-in-2 and Pay-in-6, according to a page in Affirm’s help center.

“Having all loans reflected in a consumer’s financial profile will help protect and empower borrowers,” Affirm President Libor Michalek said in the release. “The buy now, pay later industry must evolve from simply providing flexible payment options to helping consumers build their credit histories and better manage their finances, and we are pleased to be taking this step with Experian.”

The expanded credit reporting will help consumers build their credit histories and will enable both consumers and lenders to make more informed decisions, according to the release.

The new loan reporting will not be factored into consumers’ traditional credit scores in the near term, but it may in the future as new credit scoring models are developed, the release said. Read more

Klarna Lands Buy Now, Pay Later Deal with DoorDash, Notching Another Win Ahead of IPO

MacKenzie Sigalos, CNBC

Key Points

- DoorDash customers can soon buy with Klarna via full payments, interest-free installments, or deferred options aligned with payday schedules.

- For Klarna, the announcement comes after it recently became the exclusive provider of buy now, pay later loans for OnePay, the Walmart-backed fintech company.

- The partnership strengthens Klarna’s position in the U.S. just before its anticipated debut on the New York Stock Exchange.

Klarna, the buy now, pay later lender that’s headed for an initial public offering, said on Thursday that it’s signed on DoorDash as a partner, another sign of momentum for public market investors.

Klarna, the buy now, pay later lender that’s headed for an initial public offering, said on Thursday that it’s signed on DoorDash as a partner, another sign of momentum for public market investors.

It’s DoorDash’s first BNPL alliance in the U.S. and gives users of the restaurant delivery service a new way to pay for meals and products. Klarna said in a press release that DoorDash customers will be able to pay in full at checkout, split payments into four equal interest-free installments, or defer to dates that align conveniently with payday schedules.

Klarna, which is headquartered in Sweden, filed its prospectus last week to list on the New York Stock Exchange. Revenue last year increased 24% to $2.8 billion, and adjusted operating profit was $181 million, swinging from a loss of $49 million a year earlier. CNBC reported on Monday that Klarna will be the exclusive provider of buy now, pay later loans for OnePay, the Walmart-backed fintech company. Read more

Cash App Launches National Brand Campaign Inviting Customers to “Cash In” on Better Banking and Savvier Spending

Business Wire

“Cash In” is the company’s largest marketing campaign to-date that highlights the benefits of using Cash App as a primary financial services platform

“Cash In” is the company’s largest marketing campaign to-date that highlights the benefits of using Cash App as a primary financial services platform

As part of the campaign, Emmy-nominated director Ramy Youssef showcases the opportunities for customers who manage their money with Cash App in a four-part ad series

Cash App, part of Block, Inc., today announced “Cash In,” a multi-channel, national brand campaign that showcases how the growing suite of banking features available within Cash App can make customers’ money go further, without hidden fees.

“Cash In” first came to life through the company’s largest out-of-home campaign to-date, which began rolling out in February across key U.S. markets to drive Cash App adoption including New York, Atlanta, Miami, and Houston. Today, Cash App released two of four ads directed by actor, comedian, director, and screenwriter Ramy Youssef (Mo, Ramy, The Bear) titled “Tips” and “Wingin’ It.” The videos depict everyday scenarios of people using Cash App products to unlock savvier ways to save and spend, from automatically distributing a paycheck into Stocks, Bitcoin, and Savings, to making a crucial work-related purchase with the help of free overdraft coverage. Read more

Mar. 14, 2025: Technology & Payments Articles

- Senate Votes To Scrap CFPB Oversight of Big Tech Payment Apps

- Industry Survey Reveals Current Digital Technologies Adoption Rates

- House Bill Seeks to Improve Accuracy in Improper Payment Reporting

- Robinhood Paying $29.75 Million to End US Regulator’s Probes

Senate Votes To Scrap CFPB Oversight of Big Tech Payment Apps

FinExtra

The US Senate has voted to overturn a Consumer Financial Protection Bureau rule that would give the watchdog oversight of tech giants, such as Apple, Google and X, that offer digital payment apps and wallets.

Voting along party lines, the Senate backed a Congressional Review Act resolution introduced by Republicans Pete Ricketts and Mike Flood. It still needs to pass in the House of Representatives.

Finalised late last year, the CFPB rule is designed to ensure that the big nonbank players follow federal law just like large banks, credit unions, and others already under its supervision. In addition to the likes of Google, Apple and PayPal, it would likely impact X, which has outlined plans to add payment services this year.

X owner Elon Musk has been leading the Trump administration’s charge against the CFPB through the Department of Government Efficiency (DOGE). Last month he posted “CFPB RIP” with a tombstone emoji on his site. The CFPB had argued that the rule was necessary because the likes of Apple Pay and PayPal have gained significant market share in recent years without receiving the same regulatory scrutiny and oversight as traditional FS players.

Explaining his efforts to scrap the rule, Senator Ricketts says: “This one-size-fits-all solution in search of a problem unnecessarily expands the CFPB’s authority. Our legislation eliminates barriers to innovation, cuts red tape, and supports our job-creators.” Read more

Industry Survey Reveals Current Digital Technologies Adoption Rates

Tim Yalich, Wolters Kluwer/CUSO Magazine

82% Say Fully Digital Experience Is Important, Yet Only 9% Currently Offer a Full Suite of Digital Lending Experiences

82% Say Fully Digital Experience Is Important, Yet Only 9% Currently Offer a Full Suite of Digital Lending Experiences

Wolters Kluwer, a global leader in professional information, software solutions, and services, recently released the results of an industry survey of credit union executives that takes the pulse of the current environment for the adoption rate of digital transformation of back-office documents and workflow automation.

The online survey took place during the first week of May and was presented to more than 3,000 credit union executives across the U.S. The questions aimed to uncover what percentage of credit unions in the country are currently using digital tools for lending and other internal processes. However, the survey results illustrate a significant competitive gap amongst credit unions adopting and operating fully digital environments.

Most believe it’s important, but lack means

The majority of credit union executives (36%) said they are currently leveraging digital strategies and tools for digital lending experiences for members and align with internal digitized workflows. Another 32% said they offer basic digital lending (online banking) experiences for members.

Even though 82% said it is either “somewhat” or “very” important to create a fully digital experience, less than 10% of respondents (9%) said they currently offer a full suite of digital lending experiences, including banking and loan applications online. Read more

House Bill Seeks to Improve Accuracy in Improper Payment Reporting

Dave Kovaleski, Financial Regulation News

A bipartisan group of lawmakers are sponsoring a bill that seeks to strengthen transparency and accuracy in improper payment reporting.

The Improper Payments Transparency Act (H.R. 1771) would direct the President’s budget request to include the amounts and rates of improper payments at each executive agency. It would also direct the budget to have a detailed explanation of trends, and a summary of any corrective actions taken to address improper payments.

Including this data in the budget would correct the gaps in improper payment reporting. That, in turn, would streamline funding to essential government programs and reduce waste.

“Government waste and fraud continue to drain taxpayer dollars at an alarming rate, undermining public trust and fiscal responsibility. I’m proud to reintroduce this common sense, bipartisan bill to increase transparency and combat improper payments,” Rep. Rudy Yakym (R-IN), one of the bill’s sponsors, said. “The American people deserve full transparency and accountability in how their hard-earned money is spent, and this legislation is a crucial step toward ensuring responsible stewardship of taxpayer funds.”

The bill I cosponsored by Reps. Jack Bergman (R-MI), Jimmy Panetta (D-CA), and Scott Peters (D-CA).

Since 2003, the federal government has made $2.8 trillion in improper payments. In fiscal year 2023, 14 federal agencies reported a total of $236 billion in improper payments across 71 government programs. Read more

Robinhood Paying $29.75 Million to End US Regulator’s Probes

Jonathan Stempel, US News/Reuters

![]() Robinhood Markets, the online trading platform, agreed to pay $29.75 million to resolve several Financial Industry Regulatory Authority probes into its supervision and compliance practices, including failure to respond to “red flags” of potential misconduct.

Robinhood Markets, the online trading platform, agreed to pay $29.75 million to resolve several Financial Industry Regulatory Authority probes into its supervision and compliance practices, including failure to respond to “red flags” of potential misconduct.

The brokerage regulator said on Friday that Robinhood will pay a $26 million civil fine and $3.75 million of restitution to customers.

FINRA accused Robinhood of violating “numerous” rules, including a failure to implement reasonable anti-money laundering programs that caused it to miss suspicious or unauthorized trading and hackings of customer accounts.

It also said Robinhood failed to properly supervise social media influencers who promoted the company, or respond to several warnings of delays in processing trades. FINRA said the latter turned into a “severe” problem in January 2021. Late that month, Robinhood restricted trading in “meme” stocks such as GameStop and AMC Entertainment Holdings.

Restitution will go to customers who were not informed about Robinhood’s practice of “collaring” market orders, which led to some trades being canceled and reentered at inferior prices. Robinhood did not admit or deny wrongdoing in agreeing to settle, and said it has remediated the problems, which date back to 2014. Read more

Mar. 7, 2025: Technology & Payments Articles

- In A Win for Silicon Valley, Senate Votes to Overturn Key Payments Regulation That Could Benefit Elon Musk

- House Bill Seeks to Improve Accuracy In Improper Payment Reporting

- Leveraging the Payment Card to Combat Friendly and Malicious Fraud

- 75% of Financially Pressured Consumers Turn to Pay Later Plans

In A Win for Silicon Valley, Senate Votes to Overturn Key Payments Regulation That Could Benefit Elon Musk

Leo Schwartz and Jessica Mathews, Forbes

The Senate has voted to overturn key regulations that granted the Consumer Financial Protection Bureau supervision over payment services operated by platforms such as PayPal, Google, and Apple.

The largely party-line 51-47 vote on Wednesday is part of a broader campaign by the Trump administration to defang the CFPB, an agency created through the landmark Dodd-Frank financial reform of 2010 and championed by progressives like Sen. Elizabeth Warren (D-Mass.) Sen. Josh Hawley (R-Mo.) was the only Republican joining Democrats in opposing the resolution.

While the legislation must still go through the House for a vote, its passage in the Senate is a key step towards reversing the Biden-era rule, which was finalized in November. It’s a key win for trade groups representing Silicon Valley, which have long criticized the CFPB, alleging the agency had overstepped by establishing its own regulatory authority over digital payment apps like Venmo and Apple Pay.

Consumer protection advocates have raised concerns about a major conflict of interest involving any rollback. Elon Musk’s social media platform X plans to enter the payments space later this year, while Musk, through the Department of Government Efficiency, is overseeing the campaign to gut the CFPB. Read more

House Bill Seeks to Improve Accuracy In Improper Payment Reporting

Dave Kovaleski, Financial Regulation News

![]() A bipartisan group of lawmakers are sponsoring a bill that seeks to strengthen transparency and accuracy in improper payment reporting.

A bipartisan group of lawmakers are sponsoring a bill that seeks to strengthen transparency and accuracy in improper payment reporting.

The Improper Payments Transparency Act (H.R. 1771) would direct the President’s budget request to include the amounts and rates of improper payments at each executive agency. It would also direct the budget to have a detailed explanation of trends, and a summary of any corrective actions taken to address improper payments.

Including this data in the budget would correct the gaps in improper payment reporting. That, in turn, would streamline funding to essential government programs and reduce waste.

“Government waste and fraud continue to drain taxpayer dollars at an alarming rate, undermining public trust and fiscal responsibility. I’m proud to reintroduce this common sense, bipartisan bill to increase transparency and combat improper payments,” Rep. Rudy Yakym (R-IN), one of the bill’s sponsors, said. “The American people deserve full transparency and accountability in how their hard-earned money is spent, and this legislation is a crucial step toward ensuring responsible stewardship of taxpayer funds.”

The bill I cosponsored by Reps. Jack Bergman (R-MI), Jimmy Panetta (D-CA), and Scott Peters (D-CA).

“I’m proud to join Rep. Yakym in introducing this vital legislation to rein in out-of-control spending of taxpayer dollars in Washington,” Bergman said. “To get our country back on a fiscally responsible track and ensure Americans are keeping more of their hard-earned money, we must quickly eliminate waste within the federal government.” Read more

Leveraging the Payment Card to Combat Friendly and Malicious Fraud

Amanda Gourbault, Payments Journal

The Evolution of Card Payments and the Rise of Online Transactions

The Evolution of Card Payments and the Rise of Online Transactions

In the late 1990s, card payments entered a new era with the internet’s mainstream adoption. Traditionally, cardholders would swipe or dip their cards into a point-of-sale (POS) terminal in-store. This allowed some form of authentication to be carried out. However, the rise of e-commerce introduced card-not-present (CNP) transactions, where cardholders enter their details online without a physical interaction. This made it impossible for merchants to carry out in-person forms of authentication.

The Role of Zero Liability Policies in Online Card Payments

One factor that likely encouraged consumers to embrace online card payments was the protection offered by the Zero Liability policy. This ensured that cardholders were not held responsible for unauthorized charges should the card be used fraudulently, or the goods arrive incomplete or not at all. If an issue arises, consumers can initiate a chargeback process, requiring the merchant to prove that goods were delivered, and that the transaction complied with all relevant rules and regulations to avoid liability. Under certain circumstances, the liability for a fraudulent transaction will shift from the merchant to the card-issuing bank (a so-called liability shift). However, it is important to note that regardless of who is ultimately held liable, managing the chargeback process costs the issuer an average of $37 per disputed transaction.

The Surge in Transaction Disputes and Its Impact

Recently, there has been a notable increase in transaction disputes. In 2023, U.S. consumers disputed approximately 105 million charges worth an estimated $11 billion, with this number expected to rise by 40% by 2026. This surge can partly be attributed to the increasing simplicity of disputing transactions. 36% of US consumers view the ability to dispute charges in their mobile banking app as “extremely valuable.” Read more

75% of Financially Pressured Consumers Turn to Pay Later Plans

PYMNTS.com

The use of pay later plans has grown as consumers seek more flexible payment options.

The use of pay later plans has grown as consumers seek more flexible payment options.

The PYMNTS Intelligence eBook “10 Impact Statements: The 2024 Pay Later Report” explored how these installment plans are being used, who benefits from them and the reasons behind their adoption. The findings revealed key trends in consumer payment preferences and offered insights into the future of financial flexibility.

Financial Struggles Drive Pay Later Adoption

For many consumers, pay later plans are a tool for managing day-to-day expenses. Among those living paycheck to paycheck, 75% have turned to these plans within the past year. This trend is not limited to low-income households. Even consumers earning more than $100,000 annually are turning to installment plans, signaling that these options appeal across all financial levels.

Consumers who face difficulty paying bills were four times more likely to use these plans than those with a more stable financial situation, per the eBook. This suggests pay later options are not only a financial lifeline, but also a preferred choice for many consumers looking to manage their budgets.

Convenience and Rewards for Financially Stable Consumers

While pay later plans are often a necessity for those facing financial hardships, they are also appealing to more financially secure individuals. According to the eBook, 18% of non-paycheck-to-paycheck consumers used these plans primarily for convenience, with 15% also seeking rewards. Read more

Feb. 28, 2025: Technology & Payments Articles

- How Regulators, Banks, and Fintechs Can Prevent Another Synapse

- 7 Fintech and Payments Trends That Will Reshape Retail Banking in 2025

- Durbin to Reintroduce Credit Card Competition Bill

- Despite Popularity in Europe, Pay-by-Bank Still Lags in North America

How Regulators, Banks, and Fintechs Can Prevent Another Synapse

Ian Moloney, American Banker

Last spring, innovative banks, fintechs, and regulators were shaken by the collapse of prominent fintech middleware provider, Synapse.

Last spring, innovative banks, fintechs, and regulators were shaken by the collapse of prominent fintech middleware provider, Synapse.

What ensued was a maelstrom of finger-pointing, legal proceedings, and regulatory activity, ultimately leaving the industry and consumers confused and, even worse, Synapse customers without access to their funds. Nearly a year later, fintech companies, banks, and regulators must all ask themselves if they have done enough–or what more is needed–to avoid another Synapse-level disaster.

To avoid the next Synapse, three key factors must be understood. First, banks partnering with fintechs hold the ultimate liability for the activities of the fintech, even though contractually they share this responsibility. Second, banks and fintech companies should focus due diligence on whether they are a good fit rather than on a speedy onboarding process. Last, having the right regulations, people, and processes in place is essential for robust, effective risk management.

Critically important to note, however, is that in the wake of the Synapse disaster, responsible innovative banks and fintech companies have doubled down on these three points. Operationally, this means conducting proper suitability analyses and holistic qualitative and quantitative risk assessments. While these activities create additional tasks for both parties and extend the onboarding timeframe, long-term partnership success is far more preferable and prudent than the most expedient go-to-market strategy. Read more

7 Fintech and Payments Trends That Will Reshape Retail Banking in 2025

David Evans, The Financial Brand

A new report offers a comprehensive look at key payments concepts that will impact retail banks, both in the near-term and longer.

A new report offers a comprehensive look at key payments concepts that will impact retail banks, both in the near-term and longer.

Executive Summary

Retail banking is approaching a transformative crossroads with emerging fintech innovations set to disrupt traditional payment ecosystems in 2025. Major changes include Apple’s opening of NFC access creating unprecedented wallet competition, behavioral biometrics shifting to passive ID verification, and virtual cards revolutionizing B2B expense management. Regulatory developments including PSD3 readiness and regtech adoption will be critical priorities.

Forward-thinking banking executives must prepare for increased wallet competition, embrace “glocal” payment solutions, strengthen fraud prevention through AI implementation, and develop sustainability-focused offerings to maintain competitive advantage in this rapidly evolving landscape.

Key Takeaways

- Apple’s opening of its NFC ecosystem will trigger intense digital wallet competition, with traditional banks needing to develop competitive wallet offerings or risk market share erosion.

- Virtual cards will transform B2B expense management with instant issuing, spend limits, and transaction tracking capabilities that dramatically reduce fraud and manual processing.

- Behavioral biometrics used alongside static verification will create multilayered security systems with improved fraud detection and customer experience.

- Banks must embrace “glocal” payment solutions and orchestration platforms to effectively serve customers across various regions and payment preferences. Read more

Durbin to Reintroduce Credit Card Competition Bill

Lynne Marek, Payments Dive

The Illinois senator plans to reintroduce the Credit Card Competition Act proposal in a bid to increase competition for Visa and Mastercard.

The Illinois senator plans to reintroduce the Credit Card Competition Act proposal in a bid to increase competition for Visa and Mastercard.

Senate Minority Whip Dick Durbin plans to reintroduce the Credit Card Competition Act bill sometime “soon,” according to a spokesperson for his office. It’s not clear whether the Democrat will strike an alliance again on the legislation with Republican Sen. Roger Marshall, but that would seem likely, given Marshall’s strong support previously for the bill as a co-sponsor. A spokesperson for the Kansas Republican didn’t immediately respond to a request for comment.

The bill would land this year in a changed political environment with President Donald Trump now in the White House and the Senate also held by a Republican majority, giving that party control of Congress. Durbin first introduced the legislation in 2022. One of a handful of Senate Republicans who backed the bill previously was J.D. Vance, who could throw his weight behind the bill as vice president. Trump has also proposed reform for the industry by suggesting during the presidential campaign that credit card interest rates be temporarily capped at 10%.

Nonetheless, Vance reportedly had backed away from the bill at one point last year as he campaigned during the run-up to the presidential election, according to a Politico report. If the bill were to pass, banks that issue credit cards would have to ensure that for every consumer swipe there was a network available to merchants for routing the payment that wasn’t Visa or Mastercard. By requiring at least one alternative, it would presumably inject competition into a market the two networks dominate. Read more

Despite Popularity in Europe, Pay-by-Bank Still Lags in North America

Tom Nawrocki, Payments Journal

Pay-by-bank payment methods appeal to less than one-third of Canadians, except among newcomers to the country. This trend reflects a broader pattern where pay-by-bank has gained popularity worldwide—yet remains less prevalent in North America.

Pay-by-bank payment methods appeal to less than one-third of Canadians, except among newcomers to the country. This trend reflects a broader pattern where pay-by-bank has gained popularity worldwide—yet remains less prevalent in North America.