Jan. 27, ’17 NASCUS Report

Posted January 27, 2017McWatters named acting NCUA chairman;

Metsger becomes board member

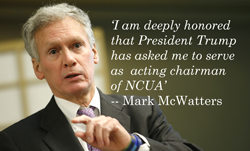

J. Mark McWatters is the new acting chairman of the NCUA Board, replacing Rick Metsger, as the result of a designation Thursday by President Donald Trump. McWatters, a Republican, has served on the board since 2014 after being nominated by President Barack Obama. His term runs to Aug. 2, 2019. Rick Metsger, a Democrat who previously served as chairman, has essentially swapped titles with McWatters, and now becomes a “member” of the board. Metsger’s term expires this year on Aug. 2.

J. Mark McWatters is the new acting chairman of the NCUA Board, replacing Rick Metsger, as the result of a designation Thursday by President Donald Trump. McWatters, a Republican, has served on the board since 2014 after being nominated by President Barack Obama. His term runs to Aug. 2, 2019. Rick Metsger, a Democrat who previously served as chairman, has essentially swapped titles with McWatters, and now becomes a “member” of the board. Metsger’s term expires this year on Aug. 2.

“I am deeply honored that President Trump has asked me to serve as acting chairman of NCUA,” McWatters said in a statement. “I look forward to continuing to work with Board Member Metsger to facilitate the ability of credit unions to better serve their members.” Metsger, also in a statement, congratulated the new acting chairman. “He and I have mutual respect for, and trust in, one another, and I think we have accomplished a good deal in the past nine months. Our commitment to working together for a safe and sound credit union system remains the same.”

NASCUS President and CEO Lucy Ito said that the selection of McWatters as acting chairman is a welcome choice to the state credit union system to lead the NCUA Board. “As a member of the board, he has displayed an intricate knowledge of the law and regulations affecting credit unions, as well as the ever-more complex accounting rules they must follow.” Ito also noted that, during the period when Rick Metsger was chairman, McWatters worked closely with the chairman in a show of solidarity and cooperation, “which we think benefited the entire credit union system.” The NASCUS leader praised and thanked former chairman (and now board member) Metsger for his leadership at the agency, and said the state system looks forward to working with him as a continuing board member.

How long McWatters serves with the “acting” designation by his name is up in the air: one seat on the three-member board still needs to be filled (it became empty when former Chairman Debbie Matz resigned last year), and Metsger’s term ends in August. Those openings give the White House some options: to nominate a Republican to fill one seat (and perhaps designate that person as chairman), or to wait and nominate a Republican and a Democrat at the same time – and name either McWatters or the new GOP representative as chairman — or something else. In any event, change is coming to the NCUA Board.

LINKS:

NCUA release: McWatters Named Acting NCUA Chairman

Statement by NASCUS President and CEO Lucy Ito

TRUMP ORDERS REGULATORY FREEZE; IMPACT ON NCUA RULES UNCLEAR

The designation of Mark McWatters as acting NCUA Board chairman could have an impact for credit unions on the regulatory freeze that President Trump imposed the day of his inauguration. The freeze, outlined in a Jan. 20 memo from White House Chief of Staff Reince Priebus to all executive departments and agencies, calls for pending regulations to be postponed for 60 days, and orders federal agencies to withdraw rules that have been proposed, but have not yet been published in the Federal Register. Priebus stated the purpose of the freeze is to ensure that Trump’s appointees or designees “have the opportunity to review any new or pending regulations.” With the designation of chairman for McWatters, the president now has a designee at NCUA.

Additionally, Priebus’ memo noted that Trump has ordered that federal agencies “send no regulation to the Office of the Federal Register (the “OFR”) until a department or agency head appointed or designated by the President after noon on January 20, 2017, reviews and approves the regulation.” As of this writing, the last word from NCUA spokesman John Fairbanks about the freeze was that the agency was “reviewing the language of the memorandum” sent by Priebus. However, since the freeze was imposed, no new regulations from NCUA (or the other federal financial regulatory agencies) have appeared in the Register.

If the “freeze” at NCUA holds, it could have some consequences for the state credit union system: the “advance notice of proposed rulemaking” on alternative capital – issued by the NCUA Board at its Jan. 19 meeting and supported by NASCUS, but still not yet published in the Register – would have to be withdrawn (for how long is uncertain). The board had assigned a 90-day comment period for the proposal. Also potentially hampered by a freeze: NCUA’s new rule on field of membership, set to take effect Feb. 6, could be held up for as much as 60 days.

In the past, when new administrations have imposed a freeze (a somewhat routine event), federal financial regulators would assert their independence, or cite an exclusion contained in the order (see following item) and continue business as usual. Both conditions may still prove to be the case, although no such specific exclusion was included in the Priebus memo. However, there may be a sign that the federal regulators are already asserting their independence: as of this writing, while a number of federal agencies have — in line with the memo — filed “letters of withdrawal” for new and proposed rules, or delayed implementation dates of new rules, none of the federal financial institution regulatory agencies have yet filed withdrawal letters for anything.

LINK:

Text of Trump regulation freeze order

HISTORICALLY, FINANCIAL REGULATORS UNTOUCHED BY FREEZE(S)

If history is any guide, the impact on NCUA and other financial regulators of the Trump regulatory freeze is … ambiguous. In many past cases, freeze orders have stated nothing when it comes to independent agencies such as NCUA and the other regulators, and the Trump memo is no different. According to Aaron Klein of the Brookings Institution, that ambiguity has left it up to the individual agencies to ignore the freeze and assert their own independence (which, he argues, was granted by Congress so that these regulators “can exercise independence from the executive branch” and to depoliticize important financial decisions – as well as to reduce “regulatory capture” by the industries they regulate). In a few cases, however, the president’s orders included an exclusion for financial regulation agencies, or “encouraged” (not required) independent agencies to comply with the orders. Last week’s regulatory freeze contained no such provisions. However, in other cases in the past, regulators have been directly affected by a freeze (including NCUA), he writes.

Klein stated his points in a blog post last week – before the Jan. 20 memo, and before a federal hiring freeze was also announced by the Trump administration on Monday. In fact, Klein’s post focused on the anticipated hiring freeze. There is, however, a key difference between the regulatory and hiring freeze: the hiring suspension notes that it applies to “all executive departments and agencies regardless of the sources of their operational and programmatic funding, excepting military personnel.” The regulatory freeze is silent in that area.

LINK:

Brooking Institution: Will Trump’s hiring freeze test financial regulators’ independence?

COURT REJECTS BANKERS’ CHALLENGE TO NEW MBL RULE

A federal court has dismissed a lawsuit against NCUA’s new member business loan (MBL) rule on procedural rules, but only after also pointing out that the suit would have been dismissed on its merits as well. The lawsuit was brought against NCUA late last summer by the Independent Community Bankers of America (ICBA, a bankers’ trade group) to invalidate and set aside a provision in the MBL rule (adopted by the agency last spring) that allows federally insured credit unions to exclude purchased commercial loans or participations in such loans from the aggregate cap on MBLs. The bankers’ group asked the court to declare that NCUA acted “arbitrarily and capriciously” and without statutory authority in concluding in the MBL rule that “to purchase a commercial loan or an interest in a commercial loan from another lender is not to ‘make’ a commercial loan within the meaning” of the law.

But U.S. District Court Judge James C. Cacheris, of the Eastern District of Virginia, did not see things as the bankers’ group presented it. “The challenged regulations reflect a reasonable interpretation of the Federal Credit Union Act,” he wrote, referring to the plaintiff’s argument that the rule violated the Administrative Procedures Act (APA). He ruled that the grievances outlined by the ICBA were not timely and that the organization lacked standing. But the judge went further: “Even if the Court was to reach the merits of Plaintiff’s APA claims, the Court would still dismiss this case.”

LINK:

Dismissal decision in bankers vs. NCUA MBL rule

ALERTS FOCUS ON HMDA REPORTING, MORTGAGE SERVICING/DEBT COLLECTION RULES

Compliance with Regulation C, the Home Mortgage Disclosure Act (HMDA) reporting, and mortgage servicing and debt collection rules, are the subjects of two “regulatory alerts” issued by NCUA this month (and summarized by NASCUS; members only). In 17-RA-01, NCUA notes that CFPB issued a final rule last summer amending certain mortgage servicing rules the consumer bureau promulgated in 2013. The alert also notes that CFPB issued an interpretive rule, which functions as an advisory opinion, on the Fair Debt Collections Practices Act (FDCPA), providing safe harbors from FDCPA liability. The final rule, NCUA stated, applies to credit unions that service first-lien mortgage loans retained in portfolio as the originator — or sold in the secondary market — but retained servicing rights. The other rule clarifies the interaction of FDCPA and certain mortgage servicing rules under Regulations X and Z (Real Estate Settlement Procedures Act and the Truth in Lending Act).

In 17-RA-02, the agency outlines reporting compliance with CFPB’s Regulation C, which implements HMDA. The alert notes that credit unions which make residential mortgage loans and meet four criteria must comply with CFPB’s Reg C – which requires the credit union to collect HMDA data associated with mortgage loan applications processed this year. “If your credit union does not meet all four criteria, you are exempt from filing HMDA data for calendar year 2017,” the alert states. The alert points out that credit unions required to collect the data must submit it to CFPB no later than March 1, 2018.

LINKS:

NASCUS Summary: 17-RA-01 (members only)

NASCUS Summary: 17-RA-02 (members only)

‘SENIOR$AFE ACT’ RE-EMERGES IN SENATE

Legislation which provides immunity from suit for certain employees of covered financial institutions who disclose or report suspected financial exploitation of senior citizens has been introduced in the Senate by Susan Collins (R-Maine) and Claire McCaskill (D-Mo.). A version of the bill, S.223 (which doesn’t yet have a title, but will likely be named the “Senior$afe Act) was passed by the House in the last Congress, but stopped short in the Senate. Under the provisions of the measure in the last Congress, a supervisor, compliance officer, or legal advisor for a covered financial institution (credit union, bank, investment advisor or broker-dealer) who has received training regarding the identification and reporting of the suspected exploitation of a senior citizen (somebody at least 65 years old) would not be liable for disclosing such exploitation if disclosure were made to a state financial regulatory agency or any of the federal financial institutions regulatory agencies, law enforcement agency, or adult protective services agency. (As of this writing, bill text for the senators’ bill was not available.)

LINK:

NASCUS Legislative Affairs web pages; ‘what we are following’

NEW BANK EXAMINING DIVISION COMMISSIONER NAMED IN S.C.

Welcome to Robert L. Davis as the new commissioner of the bank examining division of the South Carolina State Board of Financial Institutions. In his position (which he assumed Jan. 20), Davis oversees state-chartered credit unions, banks, savings and loans, savings banks and trust companies. Most recently general counsel and executive vice president for a Charleston, S.C., bank (First Financial Holdings, Inc./First Federal Bank), he has also served at the federal Office of the Comptroller of the Currency as assistant director of the enforcement and compliance division in Washington, D.C. He is a graduate of McDaniel College and the University Of Baltimore School Of Law, both in Maryland.

BRIEFLY: New members, new NCUA OSCUI leader, committee meets

NASCUS welcomes Nutmeg State Financial CU (assets: $400 million) of Rocky Hill, Conn., among its latest new members … Martha Ninichuk is the new director of NCUA’s Office of Small Credit Union Initiatives (OSCUI); she is the former deputy director of the office … the NASCUS Legislative and Regulatory Committee met Thursday and discussed pending and future issues, including establishing NASCUS’ 2017 legislative and regulatory priorities.

Information Contact:

Patrick Keefe, NASCUS Communications, pkeefe@nascus.org or (703) 528-5974

For more information about NASCUS's news and/or public relations, please contact our Marketing and Communications Department.